After a long wait, the results of the September 2017 valuation of the Social Housing Pension Scheme, or SHPS, are in. The headline is the deficit has increased to £1.5 billion. What does this mean for contributions? Guest writer, Richard Soldan, Partner at LCP, discusses.

Unsurprisingly, a bigger deficit means more contributions, starting with an additional £14m pa from next April, which is around a 10% increase on average.

Based on the current contributions agreed following the 2014 valuation, associations will have been expecting a reduction in 2020 and again in 2023, but these reductions will no longer happen. As a result, across the sector the new deficit recovery plan will mean an increase of nearly £100m pa from late 2023 onwards.

SHPS has kept the same end point for the new deficit contributions payment schedule – September 2026. Associations will need to continue to budget for these extra payments until then (and possibly longer depending on the triennial valuations in 2020 and 2023).

The increase in contributions will however vary from one association to another. SHPS is changing the way it allocates deficit contributions between employers, so it is now based on each employer’s share of overall SHPS liabilities. This seems intuitively fair, although it means some associations will see big immediate increases in deficit payments, and some could in fact see a reduction.

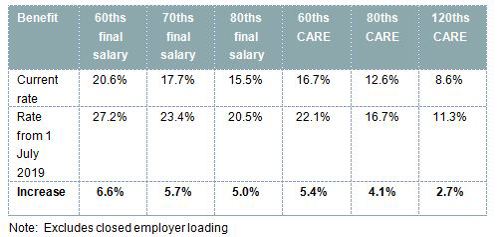

And the cost for future benefits?

The other key area where associations will see an increase in cost is the contributions associations are paying for employees who are currently earning further benefits in the defined benefit sections of SHPS – the “future service contributions”.

Across the board, aggregate contribution rates will increase by around a third from 1 July 2019.

Helpfully, for employers that have closed their defined benefit sections to new entrants the “closed employer loading” has reduced, offsetting these increases to a degree.

What can you do?

So, with increased contributions both to plug the higher deficit and to pay for future benefits, what are the options for employers in SHPS?

1. Consider the benefits you offer

The main area to manage the increase in costs will be to review the benefits provided to employees currently earning defined benefits in SHPS. In the absence of any action the entire increase in contributions would fall on employers.

The first option is to pass the increased future service contributions on to employees, and many associations already have a policy of doing so. Although with increases of up to 6.6% of pensionable salary, associations may need to think carefully about whether this is reasonable this time around.

Increase to future service contributions

Other options would be to change to a cheaper benefit scale within SHPS or to move these members to a defined contribution arrangement, where employer contributions are fixed and known. This is a step that many associations have taken in recent years, and reduces future risks as well as managing increases in cost.

As pensions is one element of an association’s overall reward package, it is important to consider how any changes fit in with other benefits and any other changes that have been or are being made.

Given the time it has taken SHPS to publish the valuation results, it is good to see they have very sensibly pushed back the increase in future service contributions to next July, and given employers until the end of April to consult with employees and decide on any changes to future benefits or contributions.

In practice this is likely to mean associations will need to start consulting with employees no later than the end of January, so we definitely expect the SHPS valuation to be on Board agendas for the next meeting.

2. Prepare the budget

When it comes to the deficit, it will be important to put the higher contributions into budgets from next April. There is an appeals process for any associations that cannot afford the contribution increases, although applications for this need to be made by the end of November.

3. Review your options

Given the change in the contribution structure, we could well see associations becoming more interested in options to manage down their liabilities in order to reduce contributions following the next valuation.

Ultimately, if associations want to take greater control of their SHPS liabilities and deficit one option is to transfer their share of the SHPS assets and liabilities to a separate pension scheme. This is a significant project, and definitely not right for all, but one that a number of high-profile housing associations have now taken.

To find out more, join our free seminar on 6 November 2018 with Sue Harvey, Partner at Campbell Tickell. Click to find out more.

For more information or to discuss this article, contact Sue Harvey on sue.harvey@campbelltickell.com

View the original blog on LCP’s site.